What Is Driving Social Inflation — and How Institutions Can Respond

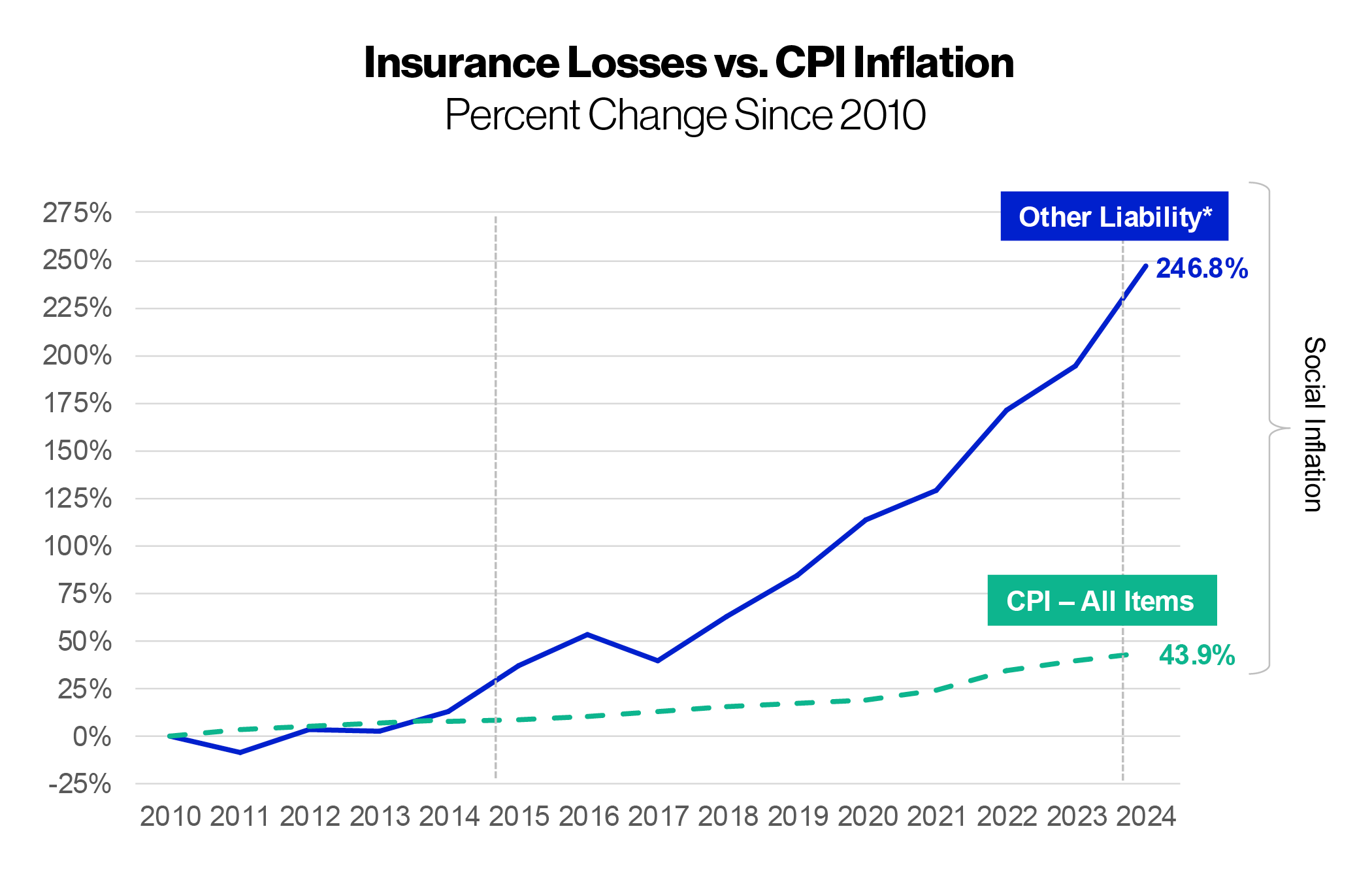

Liability Costs Continue to Outpace Inflation

Social inflation — the increased cost of litigation above general economic inflation — has significantly driven up claims costs.

While overall inflation has increased steadily, litigation-related costs have risen at a much faster pace. From 2010 to 2024, the Consumer Price Index (CPI) rose nearly 50%, compared to a 247% increase over the same period in “Other Liability,” the category in which all of United Educators’ (UE’s) lines fall.

This widening gap reflects shifts in the litigation environment, including evolving legal strategies, broader liability interpretations, and shifting public sentiment. As a result, institutions face greater financial exposure and more unpredictable claims outcomes.

At a high level, these primary factors are driving social inflation:

- A more challenging litigation environment, third-party litigation financing, increasingly plaintiff-friendly rulings, and higher jury awards and settlements

- Increased legislative risk, particularly the expansion of reviver statutes

- Institutional mistrust (the loss of trust in historically respected institutions such as educational institutions, the federal government, and news media); a recent report from Yale University examining declining trust in higher education describes the issue as “real” and “urgent,” pointing to long-term shifts in public perception

Understanding what is driving social inflation — and taking proactive steps to mitigate its impact — is critical to managing long-term risk and controlling costs.

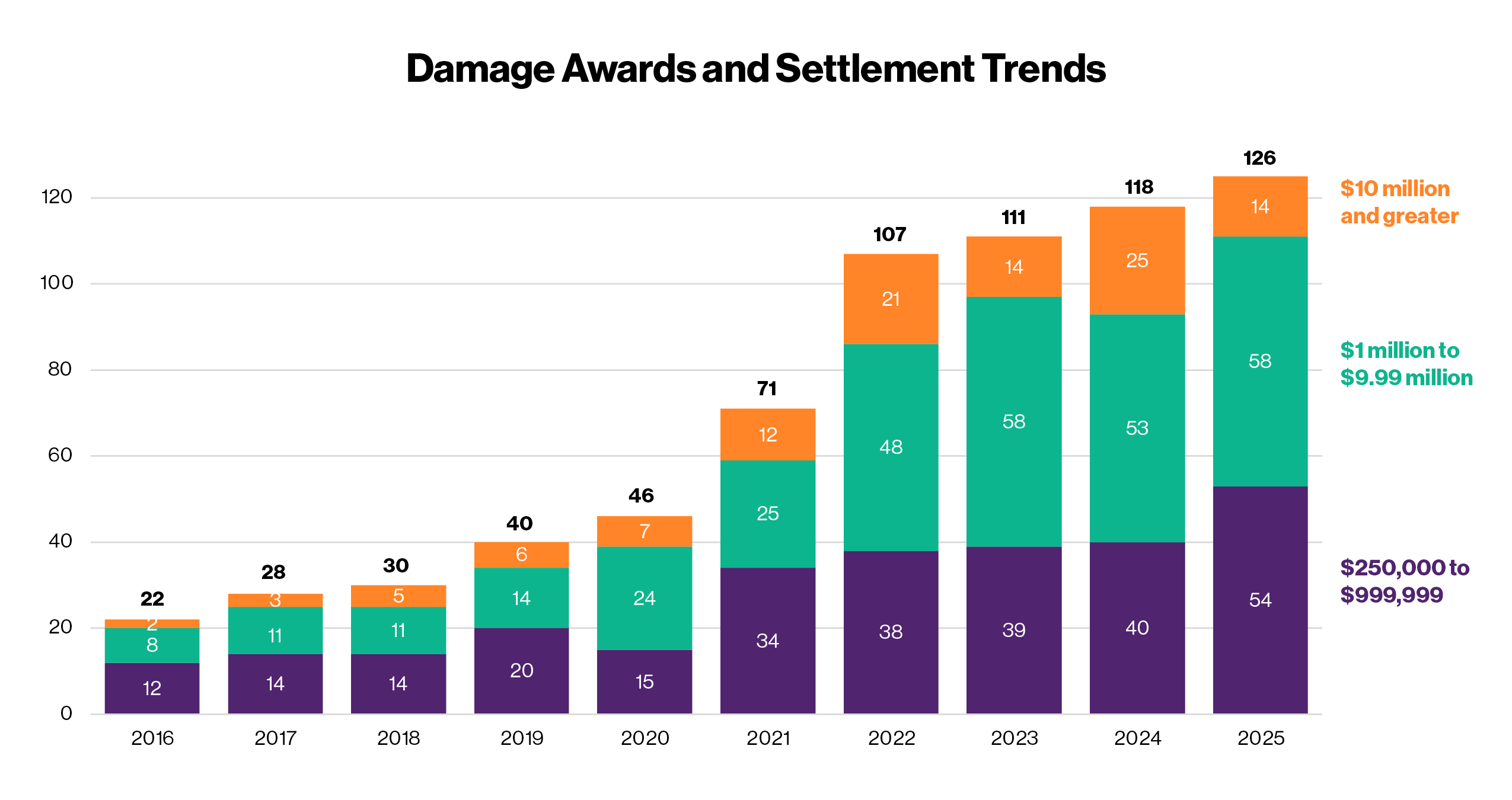

Increasing Severity and Frequency of Claims

Social inflation is driving a measurable increase in the severity and frequency of high-cost claims across the market, including educational institutions.

From 2016 through 2025, damage awards and settlements of $250,000 or more increased 473%, according to publicly reported losses for educational institutions.

UE Member Claims

From 2016 through 2025, the number of UE member matters with total incurred costs exceeding $1 million more than doubled. Notably, more claims exceeding $2.5 million were closed in 2025 than in any prior year.

Recent trends also show an increasing concentration of high-severity losses across liability lines. From 2020 to 2025, there were 43% more Educators Legal Liability (ELL) claims exceeding $1 million and 56% more General Liability Excess (GLX) claims exceeding $2 million.

From 2020 to 2025, Commercial General Liability (CGL) claim costs increased 120% (excluding child reviver act claims), contributing to significant upward pressure on both primary and excess liability coverage.

Factors Shaping Litigation Environments

A SwissRe analysis anticipates the United States will remain the epicenter of social inflation. Key factors shaping the U.S.’s litigation landscape include:

LITIGATION ADVERTISING

Trial lawyers continue to invest heavily in advertising, touting successes, and recruiting new clients for class action lawsuits. In 2024 alone, nearly 27 million advertisements soliciting legal claims were placed across television, radio, print, and digital channels, totaling $2.5 billion, according to the American Tort Reform Association. This increased visibility drives claim awareness and contributes to higher claim frequency.

THIRD-PARTY LITIGATION FINANCING (TPLF)

TPLF introduces external capital into lawsuits, with investors funding cases in exchange for a share of potential settlements or judgments. APCIA reports that TPLF accelerates loss cost trends, increasing class actions, and contributing to the potential for nuclear verdicts.

According to Westfleet Advisors, total assets under management for TPLF investments have grown to $16.1 billion.

ERODING JUROR SENTIMENT

Findings from a 2025 SwissRe study show that “juror sentiment has shifted decisively toward plaintiffs, and this shift is influencing verdicts in measurable ways.”

For example, plaintiff attorneys are employing the “Reptile Theory” trial strategy, which focuses on underlying safety or security issues in ways that appeal to jurors’ instincts for self-protection. This approach can frame institutions as bearing significant responsibility for preventing harm and encourage jurors to consider the broader implications of their verdict beyond the individual claim.

STATE REVIVER STATUTES

Reviver statutes extend or reopen the statute of limitations for certain claims, allowing cases to be filed years — or even decades — after an alleged incident. As a result, claims may arise long after policies were written, when documentation may be limited and recollections less clear.

The impact of reviver statutes is particularly evident in claims involving sexual misconduct, where extended filing windows have led to a significant increase in both claim frequency and severity.

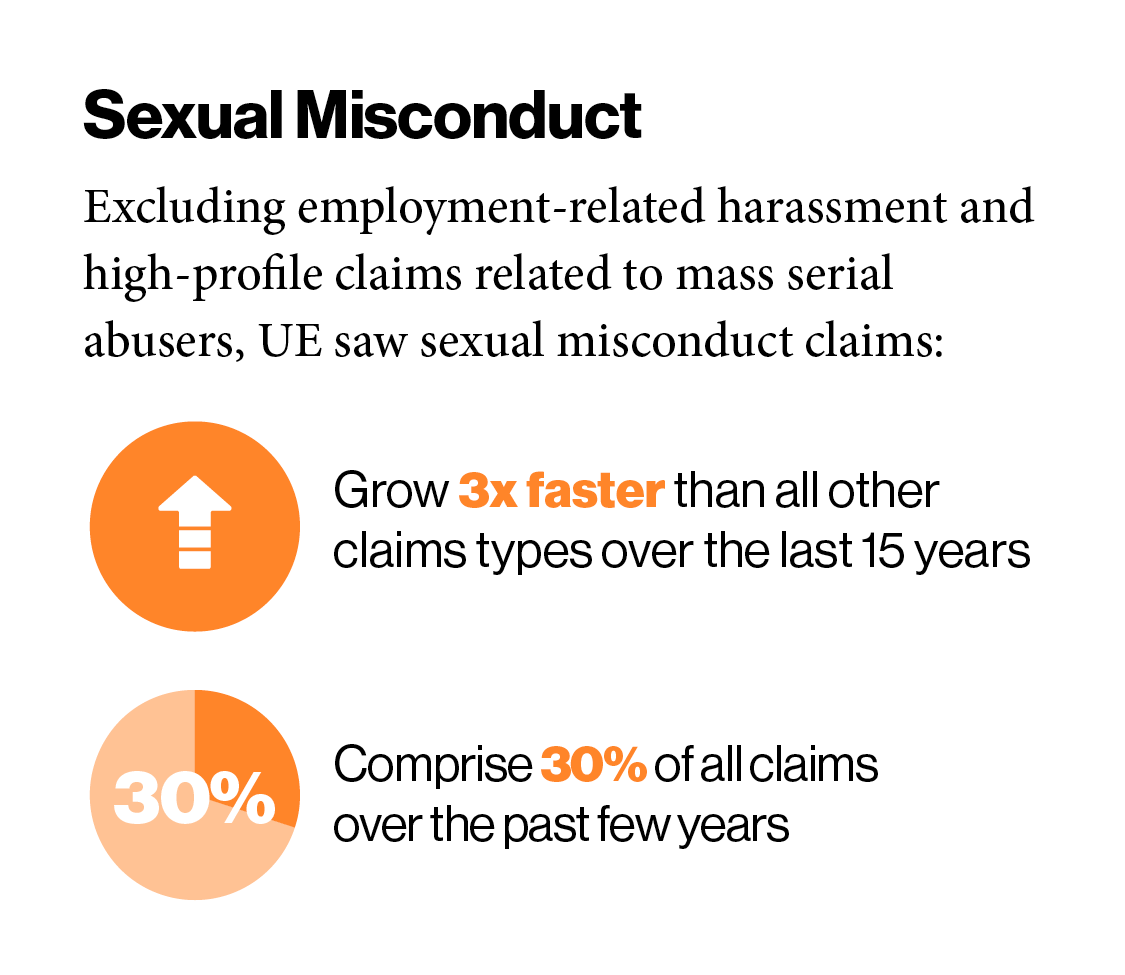

High-Cost Exposures: Sexual Misconduct and Slips, Trips, and Falls

While institutions face a range of liability risks, sexual misconduct claims represent a disproportionate share of overall losses. Over the past 15 years, these UE member claims have grown significantly — three times faster than other claim types — even when excluding employment-related harassment and high-profile claims involving mass serial abusers. They now account for approximately 30% of all member claims costs.

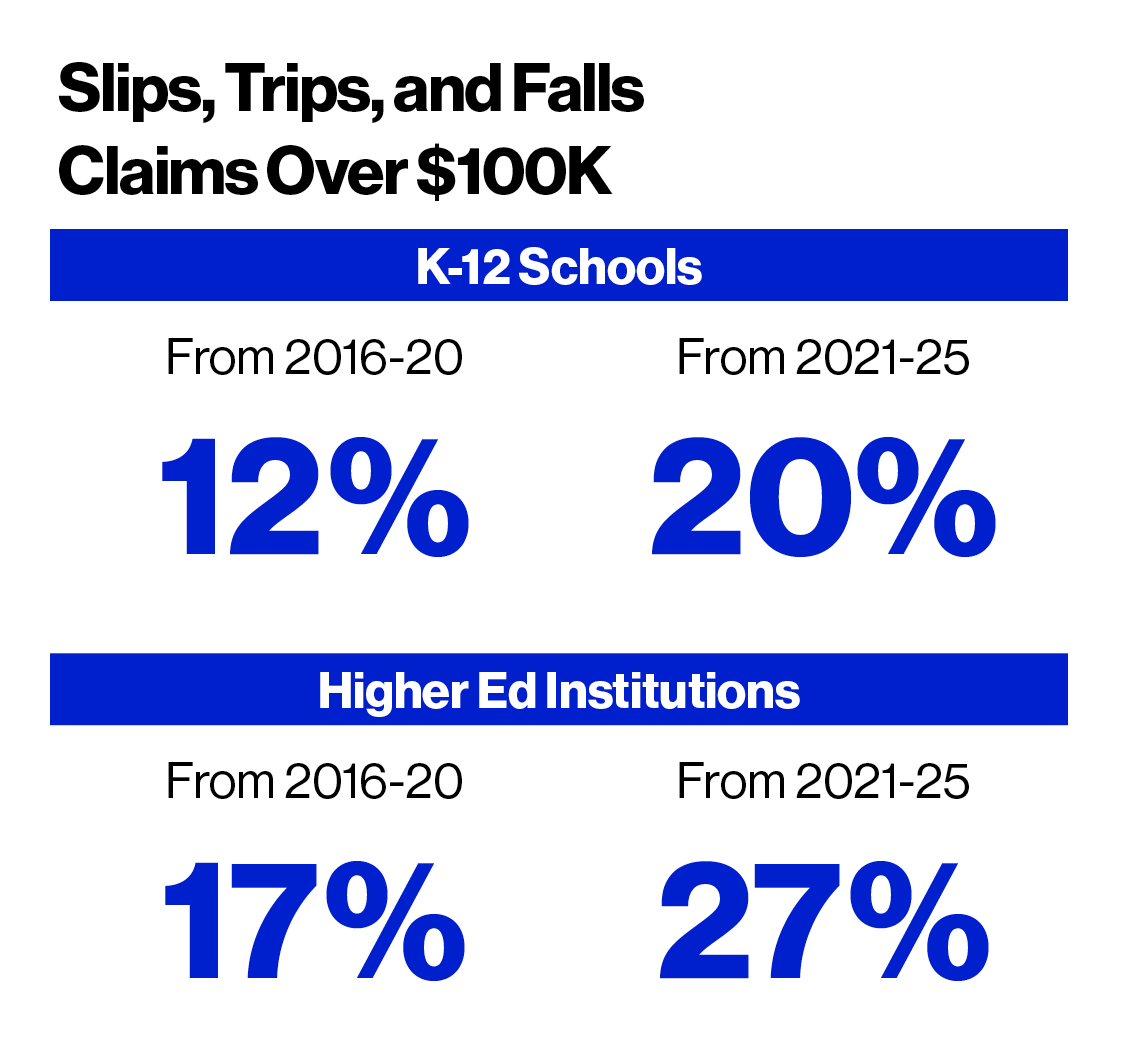

UE also has seen an increase in the severity of slip, trip, and fall claims.

For example, 20% of slip, trip, and fall claims closed at K-12 schools from 2021-25 were for over $100,000. That is compared to 12% of such claims closed from 2016-20.

At higher ed institutions, 27% of slip, trip, and fall claims closed from 2021-25 were for over $100,000. That is compared to 17% of such claims closed from 2016-20.

Slips, trips, and falls represent 33% of GL claims against higher ed institutions.

These trends highlight the need for targeted risk management, prevention, and response strategies focused on high-impact exposures.

6 Steps to Mitigate Social Inflation

Addressing social inflation requires a proactive and coordinated approach to risk management and institutional response. The following strategies, combined with UE’s resources and institutional expertise, can help reduce the likelihood and severity of claims.

1. Strengthen Risk Management Culture

Establishing a strong risk management culture is essential. Institutions should align policies, training, and oversight to proactively identify and mitigate risk across campus operations.

Periodically review campus risk management practices to ensure policies are being followed.

UE supports these efforts through education-specific resources, live risk consultants providing personalized assistance, and workshops designed to help institutions build or enhance enterprise risk management (ERM) programs.

2. Focus on High-Impact Risks

Prioritize risks most likely to result in significant financial losses.

UE works closely with members to identify top risk areas and provide targeted guidance, tools, and training to address exposures such as discrimination, sexual misconduct, and safety-related incidents. Members also can take advantage of a pre-claim advice credit, which lowers self-insured retention (SIR) when seeking early guidance from UE-selected counsel for incidents that later develop into claims.

3. Consider Options for Premium Credits

Managing financial exposure is a critical component of mitigating social inflation. Increasing SIRs or deductibles can help stabilize premiums and drive greater risk management focus on your campus. Institutions of all sizes are choosing this approach. Some charge back a portion of the deductible or SIR to individual departments or programs to encourage good risk management across campus.

UE’s Risk Management Premium Credit (RMPC) program encourages institutions to implement risk mitigation activities during the policy term. Members can earn a premium credit of up to 6% upon renewal. Participating institutions are required to address risks that drive common or significant losses related to a policy placed with UE.

Mitigation activities include training, audits, policy review and development, and tabletop exercises on high-loss topics.

4. Enhance Claims Management and Early Reporting

Early action can significantly influence claim outcomes. Prompt reporting, early case assessment, and strategic decision-making are critical to managing costs and reducing prolonged disputes.

UE’s Resolutions team brings expertise in education claims, working collaboratively with defense counsel and institutions to pursue effective, cost-conscious outcomes. This approach includes litigation management tools, case assessments, guidance on preparing proper documentation, early budget forecasting, and candid feedback.

Recognizing that prolonged disputes demand resources from all parties, UE develops strategies to explore early resolution without litigation and work collaboratively to achieve effective legal outcomes. UE’s Cool Head, Warm Heart® philosophy reflects a thoughtful, compassionate approach to claims handling.

5. Strengthen Crisis Response

An institution’s response to a crisis can directly impact both claim severity and long-term outcomes. A coordinated response that balances policy adherence with empathy and communication can reduce financial and reputational risks.

UE helps campuses strengthen readiness through crisis response tabletop exercises that assess preparedness, identify gaps, and support continuous improvement. Supplemental response services, including ProResponse®, also provide expert guidance to help communities recover.

6. Leverage UE Data, Education Expertise, and Partnership Approach

In a rapidly evolving litigation environment, institutions can benefit from ongoing access to data, analytics, and specialized expertise. Finding the right fit for defense counsel, with relevant trial experience and efficient claims management, is a key strategy to resolving claims and mitigating claims inflation.

Through its long-standing partnership with member institutions, UE provides insights into emerging risks, claims trends, and effective mitigation strategies — helping institutions stay ahead of evolving exposures and manage risk more effectively over time.

To learn more about steps you can take to mitigate social inflation, contact risk@ue.org. You also can visit ue.org/discover-ue to explore our comprehensive coverage and the full benefits of UE membership.